Industry: Aerospace and Defense

Current Dividend Yield: 2.9%

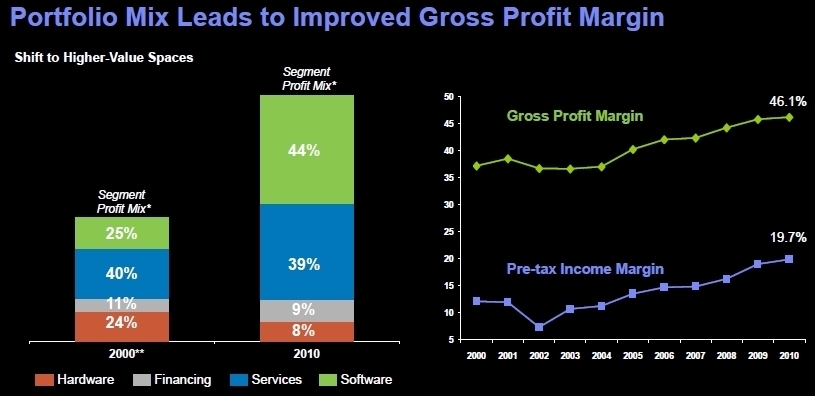

The Boeing Company is the world’s largest aerospace and defense company. It operates worldwide and is the largest exporter in the United States. Its three main divisions are Commercial Airline, Integrated Defense Systems, and Boeing Capital.

Business Segments:

Commercial Airplanes: 50%

From the iconic 747 to the all-new 787 Dreamliner, Boeing delivers a family of technologically advanced and efficient airplanes to customers around the world.[1] With a global aerospace refresh starting anew, Boeing can expect to see an increase in demand for its planes in the coming quarters. In fact, Boeing has recently received one of its largest orders to date from American Airlines. Boeing did split this order with is closest competitor, EADS NV (EADSY) but if we take management's word for it, they simply couldn’t produce enough planes to fill the order by themselves.

Integrated Defense Systems: 50%

Boeing is a recognized leader in providing and supporting large-scale systems that combine sophisticated communications networks with air-, land-, sea- and space-based platforms for military, government and commercial customers around the world.

Key IDS products are: fighter jets, rotocraft, large aircraft, missiles/bombs, satellites, communication systems, space systems and launch systems

Investors have recently been concerned with the U.S government’s contraction in defense spending. I acknowledge this is a legitimate concern, however it's not one that I am losing sleep over. The fact of the matter is that America is perpetually at war. This is not a political statement. It is what it is.

Let’s take a look at Boeing's fundamentals’:

With cyclical companies such as Boeing, it’s important to not get caught up with 7-year averages and ratios. Even with Boeing’s cyclicality, its 7-year ROE is a respectable 14.6%. Additionally, it is trading at a considerable discount to its historic P/E. Read the rest of the article here.